Thor is a myth. Wireless problems in Canada are not.

A report last week from Scotia Capital on Canada’s wireless sector caused a commotion, seeking as it did to dispel certain myths with facts. With both the government and regulators recently turning their attention to the wireless market, analyst Jeff Fan sought to tackle some of the commonly held beliefs - namely that Canadian carriers are uncompetitive and are therefore charging high prices.

Telecom consultants and the carriers themselves touted the report as proof that no additional regulation or special dispensations to new competitors are needed. “We think it is time for the regulators to declare victory on the policies they adopted five years ago,” when spectrum set-asides paved the way for new entrants, the report said.

University of Ottawa internet law professor Michael Geist fired back earlier this week with his own take. In his estimation, high prices are no myth - Canada’s wireless market is indeed “woefully uncompetitive.” Consumer advocates Open Media, meanwhile, have issued their own report, urging policy makers to fix the country’s “dysfunctional” situation.

In light of this debate, I thought it might be instructive to take a look at some of the myth-busting facts presented in the Scotia Capital report, to see if they can indeed bear the weight of closer scrutiny. It turns out that they generally can’t.

The biggest problem with the report is its insistence on comparing Canada only to the United States. I had a brief email conversation with Fan about this and I understand why he did so. The U.S. is the most similar market to Canada’s, with a common regulatory approach (as in, regulators have largely abstained from interfering) and systems. In Europe, for example, calling parties pay for calls, while in North America, minutes are counted on both the calling and receiving ends. It’s these sorts of differences that make comparing plans and prices across many countries inherently difficult.

Still, focusing only on the U.S. is aiming pretty low, considering the country has competitive problems of its own. In the first 13 years in which the Federal Communications Commission was required to submit a report to Congress, it deemed in no uncertain terms that the wireless market was competitive. That changed in 2010, when the regulator opted to refrain from making such a proclamation. The FCC didn’t go so far as to say the market was uncompetitive, but the shift in tenor was unmistakable.

The Department of Justice also felt the market was, if not already uncompetitive, very much on the verge of becoming so when it sued to block AT&T’s takeover of rival T-Mobile in 2011. That deal ultimately did not go through and antitrust watchdogs have been keeping a careful eye on the market since. That’s not the sort of market Canada should be aspiring to.

With that in mind, let’s get to those myths.

Myth #1: Canadian wireless prices are more expensive than the U.S. That’s not true, according to Scotia Capital. Smartphone plans in Canada are approximately 24 to 27 per cent cheaper across all usage categories.

This “fact” is pretty selective. For one, Virgin, Fido and Koodo are counted in the Canadian calculation, yet only Verizon and AT&T are included for the U.S. The DOJ, in its 2011 suit, characterized T-Mobile as “an independent, low-priced rival,” so why wasn’t it included in the comparison? Surely T-Mobile and number three player Sprint, with their combined 75 million or so subscribers, should have been counted. Would their numbers have moved the overall U.S. numbers downward?

It sure looks like it. As Geist points out, the number that really matters is average revenue per user - or the amount that carriers extract from each customer. Canadian carriers are pulling in an ARPU around $59 according to the Bank of America Merrill Lynch Global Wireless Matrix,* or about $8 to $9 (or 13 per cent) more than their U.S. counterparts. How are they getting more revenue per customer if their prices are supposedly lower? Unless there’s some sort of gnomish magic at work here - or selective accounting - prices are indeed higher in Canada than in the U.S.

Moreover, they are the highest in the world according to the Wireless Matrix, with ARPU projected to go even higher. Canadian carriers’ ARPU climbed 1.8 per cent in the fourth quarter of 2012, while “strong smartphone loadings, an ongoing mix shift from prepaid to postpaid, and what appears to be a more balanced pricing environment, should continue to support blended ARPU growth in the near-term,” according to a February report from Credit Suisse.

(*I’m using slightly dated figures from a 2011 version of the Global Wireless Matrix. While every effort was made to acquire the latest version, the closely guarded report is akin to the industry’s state secrets. Still, comparing against company reports and other sources, most statistics contained therein have not changed dramatically over the past year, so comparisons listed here can be assumed to be more or less accurate.)

Myth #2: Three-year contracts make Canadian plans less attractive. Actually, the Scotia Capital report says, Canadian smartphone plans are still cheaper than the U.S. even after adjusting for the higher cost on the three-year contract. Canadian plans are therefore 21 to 23 per cent cheaper, with three-year contracts apparently helping smartphone penetration in Canada.

The same magic math found in the first issue is also present here, since only Verizon and AT&T are compared. Aside from that, as Geist points out, there is no correlation between three-year contracts and smartphone adoption. If there was, countries ahead of Canada in that measure - such as Spain and the United Kingdom - would also have three-year contracts, but they don’t.

Further to that, the three-year lock-in also doesn’t take into account either the phone’s durability or the owner’s desire to keep it. If Canada truly is like the United States, then Canadians would typically be replacing their phones every 21 months. Instead, they’re stuck for an extra year, often with a phone that is positively ancient and possibly malfunctioning (ever tried to use a three-year-old iPhone? Yeesh!). Carriers might let them upgrade early, for an extra fee of course, which again is not counted in the magic math.

To address the myth head on, there’s nothing attractive about that.

Myth #3: Three-year contracts trap Canadians and should be banned. Actually, the report says, Canadian and U.S. churn rates - or the frequency with which customers defect to other carriers - are roughly the same. Churn rates should be higher in the U.S. since their contract maximums are two years.

That’s not entirely true. Going up to the point above, not only does the three-year contract prevent churn within its actual duration, it also has the effect of deflecting it even longer since subscribers are often offered (or want) “early” upgrades. But only if they sign on to another three-year contract, of course. So what should be a two-year deal often turns into a six- or even nine-year contract.

Moreover, the report is defeated by its own logic on this point. Churn in North America, according to the Global Wireless Matrix, is about 1.7 per cent, while in Europe - where three-year contracts are largely absent - it is 2.2 per cent. Those may seem like tiny percentages, but to a Canadian carrier with nine million subscribers, that’s an extra 50,000 customer defections. There’s no doubt about it: longer contracts do lock people in for longer.

Myth #4: Canadian incumbents have not been affected by new entrants. Not true, says Scotia Capital. Wireless voice ARPU has declined almost 30 per cent since 2008, total ARPU has been flat and margins fell.

This fact is mostly true. To say that Bell, Rogers and Telus haven’t been affected by the likes of Wind and Mobilicity is madness. System access fees are gone and unlimited plans are almost the norm now. You can get a half-way decent plan from the incumbents for about $60, which is a far cry from what they were charging only a few short years ago. Some have even improved their customer service.

But returning to the Credit Suisse report, incumbent ARPUs are once again climbing, with profitability (expressed as earnings before interest, taxes, depreciation and amortization) following along: “Overall, we continue to expect relatively strong growth in wireless EBITDA as the carriers leverage revenue growth combined with good cost management (expected from Rogers in particular).”

So, while incumbents have definitely been affected by new entrants, they haven’t been that affected. And the effect may only have been temporary. If revenue and profit are already starting to climb again, it’s pretty clear what the situation would have been without new entrants.

Myth #5: Higher data ARPU is due to higher prices. Higher revenue is actually the result of more people using smartphones, not higher prices, says Scotia Capital.

There might be something to that, but not according to the Global Wireless Matrix. Canadian carriers are getting around a third of their revenue from data (aka texting and smartphones), or just a little bit more than their European counterparts. Curiously, Asian carriers are getting more than half their revenue from data, yet their ARPUs are lower than Canada’s (although Japan’s is very close), which indicates the myth is actually true. Higher data ARPU is due to higher prices.

Myth #6: Canadian carriers charge more for data than the U.S. Canadian data ARPU, says the report, is similar to the U.S., ranging from $19 to $24 versus $21 to $23.

I’m not sure I’d disagree with this one, but then again, I’ve never really heard this myth before. There was a time when U.S. carriers offered unlimited data, which naturally made it much cheaper than in Canada, but they’ve been moving towards the Canadian model of smaller buckets for a while now.

Myth #7: Canada is behind because of low wireless penetration. Canada has higher smartphone penetration than the U.S. and has been outpacing its southern neighbour over the past two years.

That’s a bit of a conflation of an older myth with more recent events. Total mobile penetration - which includes non-smartphones - as a percentage of the population is around 80 per cent in Canada. According to the Global Wireless Matrix, we’re the only country in the developed world that has yet to pass the 100-per-cent mark (Japan was at 96 per cent in 2011 and has presumably passed that threshold by now). So yes, there’s no doubt we’re behind. The debate over why has been had and put to rest in 2007, when the government opted to introduce new players to the market: it’s because of historically high prices.

It’s nice to see Canada surging ahead in smartphone adoption; we’re like China, where the majority of the population skipped landlines and went straight to cellphones. Except, Canada is a supposedly advanced country.

Myth #8: Canadian wireless margins are the highest in the world. In actuality, Canadian wireless operators are not more profitable than Verizon in the United States.

If you did a double-take reading that one, you’re not alone - so did I. Verizon is indeed more profitable, but how that equates to “the world,” I’m not sure. The Global Wireless Matrix numbers show Canadian carriers to be significantly more profitable than their U.S. counterparts and in the upper echelon of the developed world. So yes, the myth is technically false, but the Scotia Capital report has a strange way of proving it.

Myth #9: Canada lags in wireless technology adoption. Factually, Canada has higher 4G LTE coverage than the U.S., the Scotia Capital report says.

That’s another myth that harkens back to a bygone era. When Rogers was the sole GSM provider in Canada, the country certainly was behind the times, with Bell and Telus licking their wounds over poorly chosen CDMA technology.

Since jointly building their new network and joining Rogers in the modern era a few years ago, nobody can say Canadians haven’t had access to the latest and greatest phones. Still, despite widespread LTE rollout, Canada isn’t faring well in global speed tests, such as the regular ones performed by content provider Akamai. Despite supposedly having some of the most advanced wireless networks around, Canada is still stuck in the slow lane. Some of this might be explained by the next “myth.”

Myth #10: Canadian wireless incumbents under-invest. Over the past five years, wireless incumbents have invested just as much as U.S. carriers.

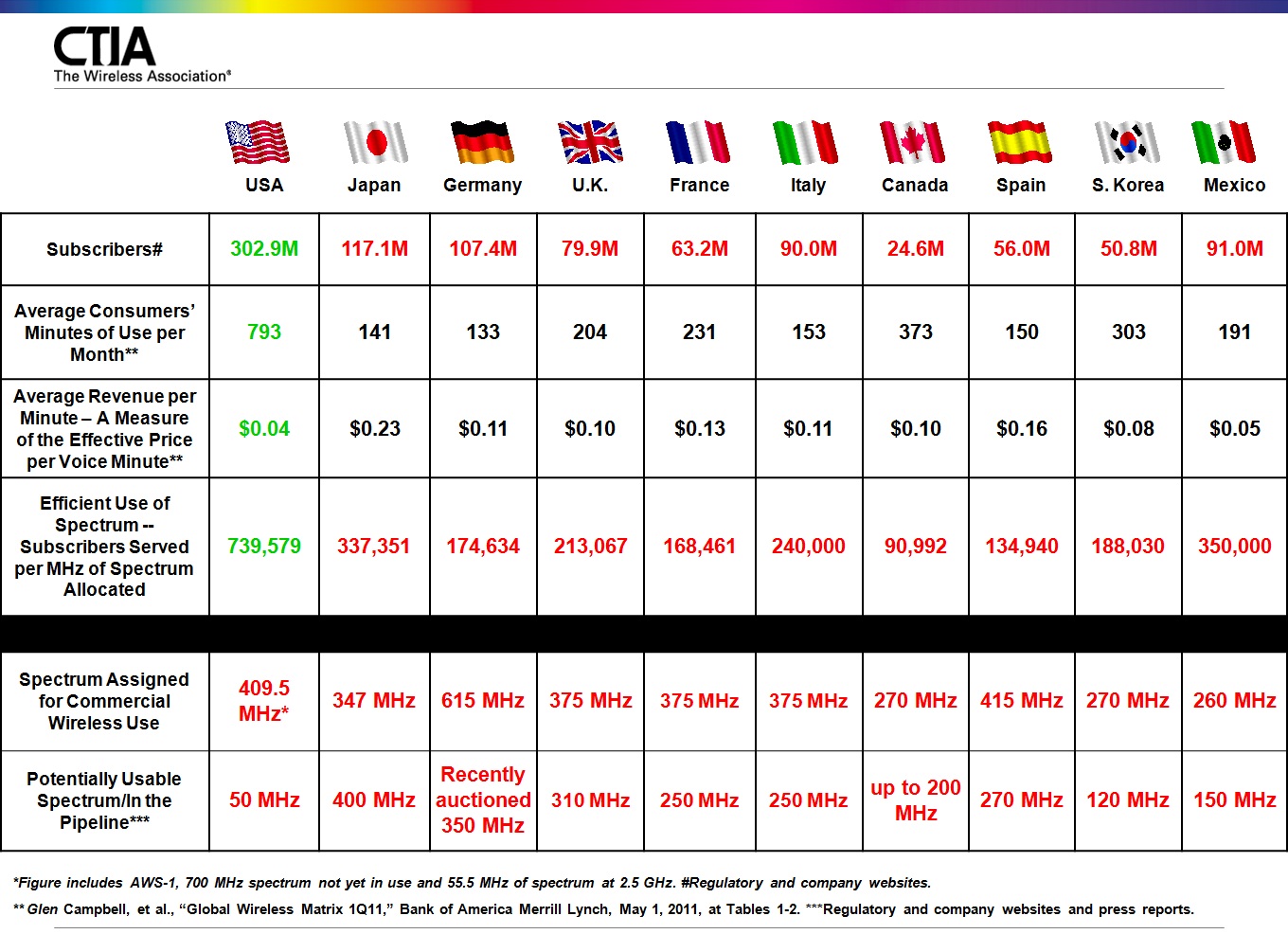

Again, that may be true, but it doesn’t mean that’s a good thing. As Geist points out, Canadian carriers are terribly inefficient at using the spectrum they have, which can be taken as an indicator of under-investment and a possible cause for those slow speeds. In a comparison of 10 countries by the CTIA, the wireless industry’s U.S. lobby group, Canadian carriers place dead last in efficiency of spectrum usage. They’re simply not building enough infrastructure to make better use of those airwaves and thus service customers better. Those same airwaves, by the way, are at the crux of this entire debate, with the government preparing to auction off another block this fall.

All told, numbers can be looked at a million different ways to show a million different results. Personally, I think Canadian policy makers should take a wider view than just looking at the United States, which itself shows signs of dysfunction. North American free marketeering is clearly not the answer; Europe’s heavier regulation might also not be the way to go. The solution, as usual, is likely something in between. That’s sort of Canada’s thing, isn’t it?

One thing that is real - that Bay Street numbers don’t capture - is the frustration and anger many Canadians have with their wireless providers. As the old saying goes, you can’t throw a stone in this country without hitting a cellphone horror story. Industry supporters try to pass this off as a small proportion of impossible-to-please complainers, but the reality is that most Canadians have unflattering feelings for their provider for one reason or another.

That’s not good or healthy for anyone. And that’s no myth.

{kind=link}

WireLESS

March 13, 2013 at 10:42 am

Churn is not a loss of a customer. It simply means that all the people pissed off with Bell go to Rogers or Telus, and vice versa. The number of contracts remains the same. There’s some small administration cost of cancelling and setting up a new account, but that’s easily recouped over the life of the contract.

The only thing I can think of why carriers fear churn is because they will have to offer lower rates to keep their customers. The rate plans remain the same, it’s just that nobody pays retail.

As for limited spending on infrastructure, absolutely true in my neighbourhood. Our cell reception has been deteriorating for two years. Rogers even admits to it and says that it’s due to the subscriber growth in our area and the congestion on the network. This is why instead of getting 3G at a respectable data rate like I used to, I’m lucky to get Edge and a data connection in my entire neighbourhood. Every time I plug my phone into the computer to sync, my computer speakers play the soundtrack from Edge (not The Edge, U2 guitarist).

I’m paying $30/month for 6 GB of data with included tethering. Almost useless since it’s impossible to use up. I used to be able to tether during a Rogers cable Internet outage but that too is impossible now. Oh, and there’s a 3-year lock-in on that even though there is no device to subsidize. And Rogers wonders why they’re nicknamed Robbers.

The nice Rogers lady who admitted to such congestion said that their technicians are looking at installing a new tower. Well, thinking about it and taking action appear to be the same thing to Rogers. I contacted the city department responsible for approvals of these towers and Rogers hasn’t applied for a new tower in our area.

It’s partially society’s fault though as we seem to fight the installation of every tower, which drags out the process and increases costs.

There are three subscribers in our family with cell phones. Between us we could come up with six to eight horror stories. Maybe cellphone penetration is only 80% in Canada, but horror stories are 280%.

Alexander Trauzzi (@Omega_)

March 13, 2013 at 12:16 pm

Canadians have earned this nightmare by either being too idealistic or too apathetic.

On one side, you have people with so much disposable income, they spoil it by setting a false standard of fairness. On the other, you have people who overextend themselves as a result of the more-money-than-brains phenomenon.

Most people will conveniently discredit this, but I think as the regard for common good has gone down in this country, so too has consumer self-respect.

If I could send one thought to all Canadians today, it might be something along the lines of “Care more!”

BT

March 13, 2013 at 12:40 pm

There is definitely some truth about prices being higher in the US.

I did the math about a month ago, comparing minimum costs for a subsidized smart phone with Rogers to the big 4 providers in the US. Over 6 years (3 contracts in the US, 2 in Canada), at advertised rates, the price difference between Rogers and AT&T/Verizon/Sprint was so much that a Rogers customer could buy a completely unsubsidized phone at the half way mark on each contract - 4 phones in 6 years instead of 3 for US customers - and still spend less money.

But there’s a pair of catches there.

First, that’s going with the cheapest plans that gets you full subsidy. None of them are terribly great value, mostly from a data cap perspective (though Sprint had unlimited data, limited everything else). The higher priced plans in the US aren’t any cheaper than Rogers - but they did tend to offer more value by comparison.

Second is that is advertised price. That’s the big one. The US carriers seem far more willing to throw around discounts and offers that shrink that advertised price than their Canadian counterparts. That’s what brings down their ARPU - they’ll give plans to you at half price if you’re persistent enough.

So for the customer willing to haggle, it’s cheaper in the US. For the customer who just takes what is listed, it’s cheaper in Canada.